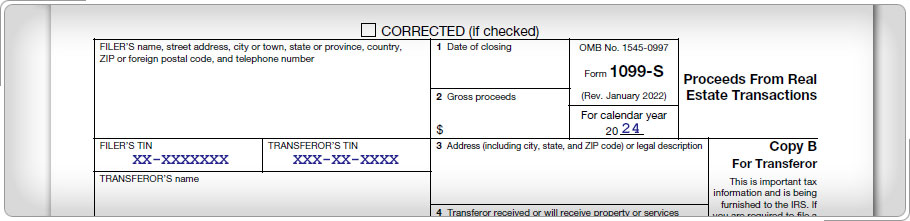

Case Study 1: Selling PriceIf the taxpayer received Form 1099-S, Proceeds From Real Estate Transactions, use it to report the selling price for the taxpayer's home. Box 1 shows the date of sale (closing) and box 2 shows the gross proceeds received from the sale of his or her main home. For taxpayers who did not receive a Form 1099-S, use sale documents and other records. If the taxpayer can exclude the entire gain from a sale, the person responsible for closing the sale (for example, a real estate broker or settlement agent) generally will not have to report it on Form 1099-S. If a Form 1099-S is issued and you determine that the gain is excludable, the sale should be shown on Form 8949 and Schedule D to notify IRS that the gain is excludable.

|